1. Introduction

Today’s post is a summer recreation/musing

about how to model the effect of

complexity and technical debt, in the same spirit of a the previous “Sustainable

IT Budget in an equation” post. I used the word “recreation” to make

it clear that this is proposed as “food for thoughts”, because I have worked

hard to make the underlying model really simple, without the intent of

accuracy. I have worked on IT cost modelling since 1998 and have removed layers

of complexity and precision over the years to make this model a communication

tool. You may see the result, for instance, in my lecture at

Polytechnique about IT costs.

This post is a companion to the previous “Sustainable

Information Systems and Technical Debt” with a few (simple)

equations that may be used to explain the concepts of sustainable development and complexity management to an audience who

loves figures and quantified reasoning. It proposes a very crude model, that

should be used to explain the systemic behavior of IT costs. It is not meant to

be used for forecasting.

What is new in this model and in this post, is

the introduction of change and the cumulated effect of complexity. The previous

models looked at the dynamics of IT costs assuming an environment that was more

or less constant, which is very far from the truth, especially

in a digital world. Therefore, I have extended this simple model of

IT costs into two directions:

- I have introduced a concept of « decay » to represent the imperative for change. I am assuming that the value delivered by an IT system decreases over time following a classical law of “exponential decay”. This is a simple way to represent the need for « homeostasis », which is the need to keep in synch with the enterprise’s environment. The parameter for decay can be adjusted to represent the speed at which the external environment evolves.

- I have also factored the effect of cumulated complexity into the model, as a first and simple attempt to model technical debt. This requires modelling the natural and incremental rise of complexity when IS evolves to adapt to its environment (cf. previous point) – as noticed before, there is a deep link between the rate of change and the importance of technical debt – as well as the representation of the effort to clean this technical debt.

This model makes use of Euclidean

Scalar Complexity(ESC), a metric developed with Daniel Krob and

Sylvain Perronet to assess integration complexity

from enterprise architecture schema. ESC is easy to compute and is (more or

less) independent from scale. The

technical contribution of this new model and blog post is to propose a link

between ESC and technical debt. Although this link is somehow naïve, it

supports “business case reasoning” (i.e., quantifying common sense) to show

that managing technical debt has a positive long-term return on investment.

This post is organized as follows. Section 2

gives a short summary of asset management applied to information systems, in

other words, how to manage information systems through replacement and

renovation rates. This is the first systemic lesson: investments produce assets

that accumulate and running costs follow this accumulation. The proposed

consequence is to keep the growth and the age of the assets under control.

Section 3 introduces the effect on computing (hardware) resource management on

IT costs. We make a crude distinction between legacy systems where hardware is

tied to application in a way that required a complete application

re-engineering to benefit from better generations of computing resources, as

opposed to modern virtualized architecture (such as cloud computing) that

supports the constant and (almost) painless improvement of these resources.

This section is a simplified application of the hosting cost model proposed in

my second book, which yields similar results, namely that Moore’s

law benefits only show in IT costs if the applicative architecture makes it

possible. Section 4 introduces the need for change and the concept of

exponential decay. It shows why managing IT today should be heavily focused on

average application age, refresh rate and software asset inertia. It also

provides quantitative support for concepts such as multi-modal

Information Systems and Exponential

Information Systems. Section 5 is more technical since we introduce

Information System complexity and the management of technical debt from a

quantified perspective. The main contribution is to propose a crude model about

how complexity increases iteratively as the information system evolves and how

this complexity may be constrained through refactoring efforts at the

enterprise architecture level. Although this is a naïve model, at a macro

scale, of technical debt, it supports quantified reasoning which is illustrated

throughout this blog post with charts produced with a spreadsheet.

2. Asset Management and Information Systems

We will introduce the model step by step,

starting with the simple foundation of asset management. At its simplest, an information system is a set of software assets that

are maintained and renewed. The software process here is very

straightforward: a software asset is acquired and integrated into the

information systems. Then it generates value and costs: hosting costs for the

required computing assets, support costs and licensing costs. The previously

mentioned book gives much more details about the software assets TCO; this

structure is also found in Volle

or Keen

. The software lifecycle is made of acquisition, maintenance, renewal or kill.

We will introduce the model step by step,

starting with the simple foundation of asset management. At its simplest, an information system is a set of software assets that

are maintained and renewed. The software process here is very

straightforward: a software asset is acquired and integrated into the

information systems. Then it generates value and costs: hosting costs for the

required computing assets, support costs and licensing costs. The previously

mentioned book gives much more details about the software assets TCO; this

structure is also found in Volle

or Keen

. The software lifecycle is made of acquisition, maintenance, renewal or kill.

Since the main object of the model is the set

of software assets, the key metric is the size of this asset portfolio. In this

example we use the Discounted Acquisition Costs model, that is the sum of the

payments made for the software assets that are in use (that have not been

killed) across the information system’s history. The IS budget has a

straightforward structure : we separate the build costs (related to the

changes in the asset portfolio : acquisition, maintenance, etc.) and the run

costs (hosting, support and licensing). Run costs are expressed directly as the

product of resource units (i.e. the size of the IS / software assets) and unit

costs (these unit costs are easy to find and to benchmark).

The model for the Build costs is more elaborate

since it reflects the IS strategy and the software product lifecycle. To keep things as simple as possible we

postulate that the information system strategy in this model is described as an

asset management policy, with the following (input) parameters to the model:

- The total IT budget

- The percentage of Build budget that is spent on acquiring new assets (N%)

- The percentage of Build budget that is spent on retiring old assets (K%)

- The percentage of Build budget that is spent on renewals (R%)

With these four parameters, the computation of

each yearly iteration of the IT budget is straightforward. The run costs are

first obtained from the IS size of the previous year. The build budget is the

difference between total IT budget and run costs. This build budget is

separated into four categories: acquiring new assets, killing existing (old)

assets, replacing old assets with newer ones (we add to the model an efficiency

factor which means that renewals are slightly more efficient than adding a brand-new

piece of software) and “maintenance”. Maintenance (for functional or technical

reasons) is known to produce incremental growth (more-or-less, it depends on

the type of software development methodology) which we can also model with a

parameter.

The model is,

therefore, defined through two key equations which tells how the asset

portfolio changes every year in size (S) and age (A). Here is a simplified description (S’ is the

new value of “assets size”, S is the value for the previous year):

- Growth of the assets: S’ = S - Build x K% + Build x A% + Build x (1 – K% – A% – R%) x G%

- Ageing of the assets: A’ = (A + 1) x (S – Build * (1 – N% - R% - K%)) / S’

Measuring software assets with Discounted

Acquisition Costs has benefits and drawbacks. The obvious benefit is that it is

applicable to almost all companies. The value that is used for discounting with

age has a small effect on the overall simulation (and what will be said in the

rest of the post). Typical values are between -3% to -10%. The drawback is that

money is a poor measure of complexity and richness of the software assets. A

better alternative is to use function points, but

this requires a fair amount of efforts, over a long period of time. When I was CIO

of Bouygues Telecom, I was a strong proponent of function points but I found it

very hard to make sure that measurement was kept simple (at a macro scale) to

avoid all the pitfalls of tedious and arguable accounting. What I have found

over the years is that it is almost impossible to use function points without

strong biases. However, as soon as you have a reasonable history, it works very

well for year-by-year comparisons. Used at a macro scale, it also gives good

benchmarking “orders of magnitudes”.

There are many other alternatives (counting apps, databases, UI screens,

….) that suffers from the same benefits and drawbacks. Since I aim to propose

something generic here – and because discussing with CFOs is a critical goal of

such a model -, using DAC makes the most sense.

The

following chart gives an example of simulating the same information system,

with the same constant budget, under three strategies:

- The “standard strategy” is defined by N% = 5%, K% = 3%, R% = 50%. With 50% of the project budget spent on renewal, this is already a strong effort to keep the assets under control. The imbalance between what needs to be added (5% of the budget to meet new needs and a small effort for decommissioning) is quite typical.

- The “clean strategy” is defined by N% = 5%, K% = 8%, R%=60%. Here we see the effect of try to clean up the legacy (more renewal effort, and more decommissioning).

- The “careless” scenario is defined by N% = 5%, K% = 3% and R% = 30%. This is not a large change compared to the standard one, less effort is made on renewing assets so that more money can be spent on adapting the existing assets to the current needs.

These three

figures illustrate some of the key lessons that have been explained before, so

I will keep them short:

- Changes that may seem small in the strategy (the values from the three scenarios are not all that different) produce significant differences over the years. Especially the “Build/Run” ratio changes significantly here according to the strategy that is picked.

- Beware of accumulation, both in size and ageing, because once the problem accumulates it becomes hard to solve without a significant IT budget increase.

- The effects of an aggressive cleanup asset management strategy are visible, and pay for themselves (i.e., they help free build money to seize new opportunities), but only after a significant period of time, because of the multiplicative effects. Therefore, there is no short-term business case for such a strategy (which is true for most asset management strategies, from real estates to wine cellars).

As I will explain in the conclusion, showing

three examples does not do justice to the modelling effort. It is not meant to

produce static trajectories, but rather to be played with in a “what if” game.

Besides, there are many hypotheses that are specific to this example:

- The ratio between the Build budget and the value of the asset portfolio is critical. This reflects the history of the company and differentiates between companies that have kept their software assets under control and those where the portfolio is too large compared to the yearly budget, because accumulation has already happened.

- This example is built with a flat budget, but the difference gets bigger if there are budget constraints (additional project money is “free money” whereas “less project money” may translate to forced budget increase because renewing the SW assets is mandatory for regulatory reasons … or because of the competition).

- The constants that I have used for unit costs are “plausible orders of magnitudes” gathered from previous instances of running such models with real data, but each company is different, and the numbers do change the overall story.

- We do not have enough information here to discuss about the “business case” or the “return on investment” for the “cleanup strategy”. It really depends on the value that is generated by IT and the “refresh rate” constraints of the environment, which is what we will address in Section 4.

3. Managing Computing Infrastructures to Benefit Moore’s Law

In the previous model I have assumed that there

is a constant (cf. the unit cost principle) cost of hosting a unit of software

asset on computing resources. This is an oversimplification since hosting costs

obviously depends on many factors such as quality of service, performance

requirement and software complexity. However, when averaged over one or many

data centers, these unit costs tend to be pretty “regular” and effective to

forecast the evolution of hosting. There is one major difference that is worth

modelling: the ability to change, or not, the computing & storage hardware

without changing the software asset. As explained in my second book, “Moore’s Law

only shows in IT costs if it is leveraged”, that is if you take advantage

of the constant improvement of hosting costs. To keep with the spirit of a

minimal model, we are going to distinguish two types of software:

- Legacy: when the storage/computing configuration is linked to the application and is not usually changed until a renewal (cf. previous section) occurs. In this case, unit costs tend to show a slow decline over the years, due to automation and better maturity in operation, which is very small compared to the cost decrease of computing hardware. This was the most common case 20 years ago and is still quite frequent in most large companies.

- Virtualized: when a “virtualization layer” (from VM, virtual storage to containers) allows a separation between software and computing assets. This is more common nowadays with cloud (public or private) architecture. Because it is easier to shift computing loads from one machine to another, hosting costs are declining more rapidly. This decline is much slower than Moore’s law because companies (or cloud providers) need to amortize their previous investments.

This split is easy to add into our asset model.

It first requires to track software assets with two lines instead of one

(legacy and virtualized), and to create two set of unit costs (which will

reflect the faster reduction for virtualized hosting cost, as well as the

current difference which is significant for most companies since virtualized

load tend to run on “commodity hardware” whereas legacy software often runs on

specialized and expensive hardware (the most obvious example being the

mainframe).

The software asset lifecycles are coupled as

follows. First the kill ratio K% must be supplemented with a new parameter that

says how much of the effort is made on the legacy portfolio compared to the

virtualized one. Second, we assume here – for simplification – that all

applications that are renewed are ported to a newer architecture leveraging

virtualized computing resources. Hence

the renewal parameter (R%) will be the main driver to “modernize” the asset

portfolio.

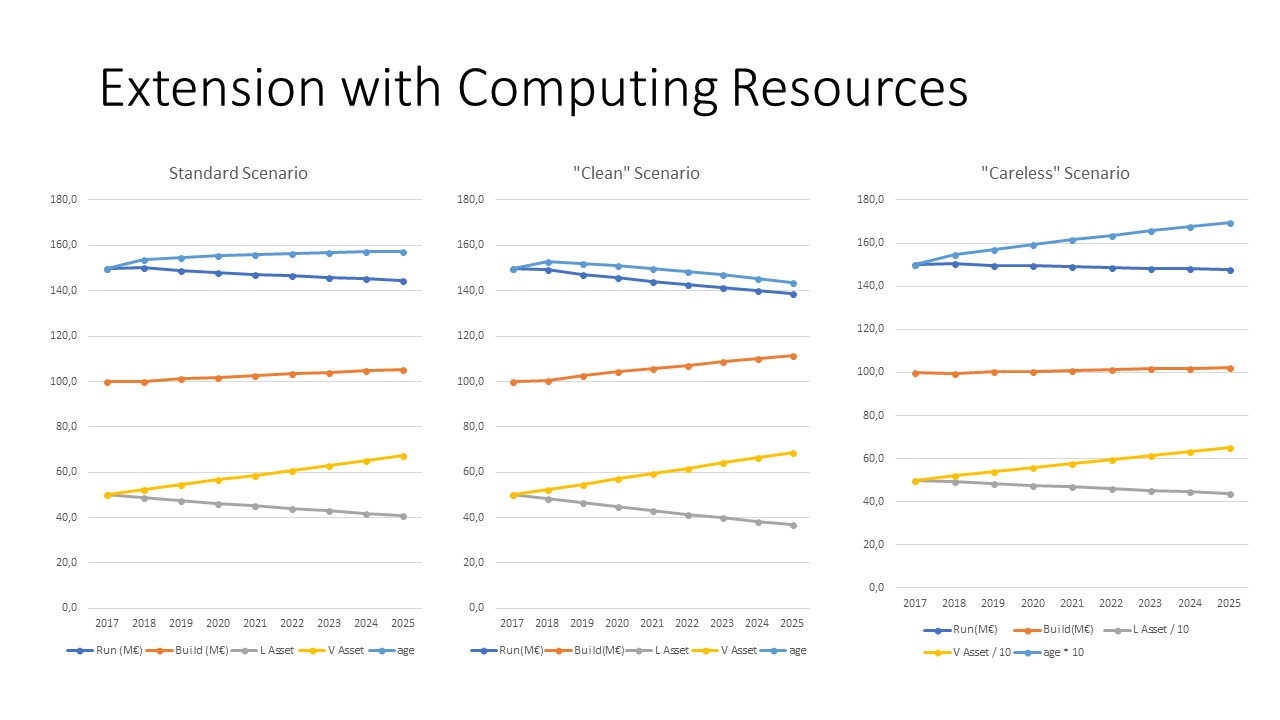

The following curves show the difference

between three strategies, similarly to the previous section. We have taken a

generic example where the portfolio is balanced at first between legacy and

virtualized computing architecture. In this run, the new ratio (N%) is raised

to 10% to reflect a situation where more change is required. The difference is

mostly about the renewal rate (respectively 40%, 50% and 30%) and the kill rate

(respectively 3%, 5% and 3%). The figure shows the size of the two software

asset portfolios (Virtualized and Legacy) as well as the average age.

The model was run here with conservative costs

estimates on purpose. The reader is encouraged to run this type of computation

with the real values of unit cost that s/he may observe in her company. Even

with this conservative setting, the differences are quite significant:

- A sustained renewal effort translates into a more modern portfolio (the difference in average age is qui significant after 8 years) and lower run costs. It is easy to model the true benefits of switching to commodity hardware and leveraging virtualization.

- The difference in the Build/Run ratio is quite high, because the run costs are much lower once a newer architecture is in place.

- These efforts take time. Once again, the key “strategic agility” ration is “build/run”. When the asset portfolio has become too large, the “margin for action” is quite low (the share of the build budget that can be freely assigned to cleanup or renewal once the most urgent business needs have been served).

To make these simulations easier to read and to

understand, we have picked a “flat IT budget scenario”. It is quite interesting

to run simulations where the “amount of build project” has a minimal value that

is bound to business necessities (regulation or competition – as is often the

case in the telecom market). With these simulations, the worse strategy

translates into a higher total IT cost, and the gap increases over the years

because of the compounded effects.

4. Managing Information Systems Refresh Rate to Achieve Homeostasis

I should apologize for this section title which

is a mouthful bordering on pretentious … however I have often used the concept

of “homeostasis” in the

context of digital

transformation because it is quite relevant. Homeostasis refer to the

effort of a complex systems (for instance a living organism) to maintain an

equilibrium with its environment. In our world of constant changes pushed by

technology rapid evolution, homeostasis refers to the constant change of the information

system (including all digital assets and platforms) to adapt to the changing

needs of customers and partners. From my own experience as an IT professional

for the past 30 years, this is the main change that has occurred in the past decade:

the “refresh rate” of information systems has increased dramatically. This is

an idea that I have developed in many posts

from this blog.

This is also a key idea from Salim Ismail’s

best seller book “Exponential

Organizations” which I have used to coin the expression “Exponential

Information Systems”. From our IT cost model perspective, what this says is

that there is another reason – other than reducing costs and optimizing TCO –

to increase the refresh rate. I can see two reasons that we can to capture:

first, the value provided by a software asset declines over time because the

environment changes. Second, no software asset is isolated any more, each is part

of a service (or micro service) orchestration patterns, that comes with its own

refresh rate constraints. I have found that the best way to express both

principles is to postulate that the value provided by a software asset declines

over time following a classical exponential decay

law:

Value = V0 x exp(- lambda x time)

This formula is easy to introduce in our model,

and it adds a penalty to ageing software that is independent from the previously

mentioned TCO effects on licensing, maintenance, or hosting. The

decay parameter (lambda) is a way to tell the model that “software must change

regularly” to cope with the constant changes of its environment.

I will not offer any simulation or charts here,

because it is actually quite difficult to find data about this “decay” (need

for change) and it makes little sense to invent one for a generic simulation. Also,

not all software assets are equal with respect to exponential decay.

Software-as-a-service (SaaS) is precisely an answer to this need for constant

adaptation. Therefore, should we plan to run simulations seriously, we should

use different decay constants for different classes of assets. There are plenty

of software costs benchmarking materials that may be used to calibrate or

evaluate the unit costs for the two previous models but evaluating the “rate of

decay” is much more difficult and very specific to each industry.

On the other hand, exponential decay / forced

rate of change is a really useful concept when planning about the long-term

future of information systems. When one plays with the previous model augmented

with decay, it becomes clear that the

desired rate of change, which is a business imperative, is not compatible with

the inertia that is exhibited by the model. This should be clear in the

example shown in the previous section: the weight of the legacy portfolio is

too high to obtain a homogeneous high refresh rate. In most large and

established company, the Build/Run ratio is worse that what is proposed here,

which means that the ability to increase the refresh rate is even worse.

This situation yields naturally to the concept

of “multi-modal IT”, including the famous “bimodal IT”

pattern. A multi-modal information

system is organized in an “onion structure” with a core and layers towards the

periphery. Using API (Application

Programming Interfaces), the onion may be organized so that the refresh

rate is higher in the outside layers than in the core. This a direct

application from biology and a pattern that is used in many organization theories

such as betacodex. This is also the foundation for Exponential

Information Systems: Use Enterprise

Architecture and modularity to support different refresh rates for different

parts of the information systems. The core/shared/pivot/common data model,

that described the key business objects that are used throughout the multiple

layers (multi-modal component) is a critical component of the Enterprise

Architecture since it defines the agility through the API. A modular multimodal

architecture is one that leaves most of the changes in the layers that were

designed to accommodate high refresh rates. This means that modularity is a dynamic

property of system architecture much more than a static one.

The lesson from this short section is that one

should think really hard about the required refresh rates of sections of their

information systems. For each functional domain, a target refresh rate (which

is equivalent to a target average age for software assets) should be set. This

target is both a business and technical imperative which should be based on

requirements from customers and partners, as well as constraints related to

software ecosystems. Many software environments, such as developing a mobile

application, come with their own refresh rate constraints because the key

features provided by the ecosystem change constantly … while upward

compatibility is approximate at best. Similarly, the ambition

to leverage artificial intelligence and machine learning for a given

business domain should translate into setting a high refresh rate target. Keep

in mind that adapting to the outside environment is a business imperative: if the lack of architecture modularity and

the inertial of the accumulated weight of the asset portfolio prevent from

upgrading the portfolio fast enough, the obvious solution is to grow this

portfolio resulting in added complexity and IT costs.

5. Information Systems Complexity and Technical Debt

This last section introduces complexity and its

effect on TCO in our IT cost model. We have seen throughout this post that the

accumulation of weight is a burden, we shall now see that the accumulation of

complexity is also a handicap that translates into additional costs, namely

integration, testing and support costs. Obviously, the complexity of

information systems reflects the complexity of their mission and the complexity

of their environment. Somehow, this complexity is where part of the business

value and differentiation is created. What we want to focus on here is the

excess of complexity, which is precisely the definition of technical

debt.

To introduce complexity in our model, we need a

way to define and measure it. We shall use “Euclidean Scalar Complexity” because it is easy to understand and

has a set of unique properties that makes it the best candidate for managing

complexity at the Enterprise Architecture scale. The principle is quite simple.

Assume that you have an architecture schema of your information systems, with

boxes and links. Assume that you have a weight w(b) for each of the boxes, and that the existence of a link on

your schema represents an interaction between the two subsystems represented by

the box. The weight could be the DAC

measure of Section 2, the function points, or any additive metric that you like

(i.e. w(a+b) = w(a) + w(b)). The

Euclidean Scalar Complexity (ESC) of your architecture (abstraction of your

system) is the square root of the sum of:

w(x) x w(y) for all pairs of

boxes x, y that are either identical

or joined with a link on the architecture schema. Normalized ESC means dividing

the ESC value by the weight of the information systems, which yields a

complexity ratio that we shall use in our model, a number between 0 and 1 (1

means that everything is connected and a value close to zero means that every

piece is independent).

ESC is one of the few metrics that is “scale

invariant”, which is the first requirement for working at the whole IS schema

(each architecture schema is a crude abstraction) – see the 2007 paper “Complexité des systèmes d’information: une

famille de mesures de la complexité scalaire d’un schéma d’architecture”

by CASEAU Y., KROB D., PEYRONNET S. Being

scale invariant means that if a change of scale is applied to the

representation (more boxes and more links to represent the same information at

a different scale), the complexity does not change. Another short introduction

to ESC is provided in my Polytechnique

lecture. There is no need to understand ESC in detail to see how it can be

used to extend our IT cost model to manage technical debt, but the key insight

that can help is to see that ESC is foremost a (static) modularity measure. ESC

works well because it captures the benefits of Enterprise Architecture patterns

such as gateways, integration buses, API encapsulation, etc. ESC is a great

metric to capture the complexity of micro-service architectures.

As explained earlier, we do not suppose that

the ideal information system has no complexity, but rather that for a given set

of assets, there exists two complexity ratios, Cmin and Cmax, that represent on

the one hand the minimal achievable ESC (i.e. rebuilding the IS from zero using

the maximal possible modularity) and on the other hand, the complexity that one

would get by randomly adding and integrating software assets incrementally. We

used the normalized ESC, so these two numbers are between 0 and 1. Not all

architecture problems are equal: some information systems are easy to build

which translates into Cmin and Cmax being close. On the other hand, for many

systems, the difference between Cmin, Cmax and C (the actual ESC ratio) is

quite high. These two anchors makes possible the definition of technical

debt as: w(S) x (C – Cmin) / (Cmax – Cmin)

Introducing technical debt into our cost model

means two things:

- Measuring the impact of this additional complexity on costs.

- Defining and measuring what “reducing the technical debt” (i.e., managing complexity) may mean, in terms of effect and cost.

The first part is easy, considering the

simplicity of our model and the fact we are just looking for simple orders of

magnitude. In a same way that we have take the effect of aging into account for

licensing, we upgrade the following formulas:

- Integration costs are proportional to the ESC : for a project with no complexity at all it would be zero (negligible compared to the cost of building / buying the new component) whereas for a truly complex (C = 1.0) system, integration (and testing) costs are equal to the acquisition costs. This is very debatable (because it is so simple and because integration costs may be even worse) but it gives a first plausible value.

- Support costs are also impacted: a fraction of support costs is proportional to C. This fraction is different for each information systems and depends on the nature of support activities (for instance, level 1 support is less impacted than level 3 support). Thus, this fraction is left as a model parameter.

The second part is the true extension of the

model and what makes this post a new contribution to IT cost modelling.

- Complexity without any refactoring effort evolves naturally towards Cmax as an asymptotic value (which is the definition of Cmax). The speed of evolution depends on how much of the information system is renewed each year, so the resulting complexity is a weighted average of the previous one and Cmax, where the weights are respectively the size of what is untouched in the portfolio and the size of what is added.

- Refactoring is seen as a fraction of the renewal budget applied to reducing the complexity. The effect is described by a power law (declining return of the invested money). The maximal effect (the asymptotic value) is getting the complexity to Cmin (also by construction). I have used a power law with degree 4 which seems to reproduce the empiric observation that the refactoring efforts have a law of strongly diminishing returns (the last 60% benefits cost 80% of the effort).

The following illustration compares three IT

strategies while taking technical debt into account. In this example we assume

Cmin = 0.3 and Cmax = 0.6, with C = 0.5 at present time. The new parameters

compared to section 1 are the amount of refactoring (F%) and how much of the

kill effort is targeted towards legacy (small effect since the kill effort is

small here).

- The “standard strategy” is defined by N% = 5%, K% = 3%, R% = 40% and F%=15%. Here 40% of the project budget is spent on renewal, and 15% of that money is reserved for refactoring. 70% of the kill effort is targeted towards legacy. The ESC ratio evolves from 0.5 to 0.489.

- The “intense strategy” is defined by N% = 5%, K% = 5%, R%=50% and F= 30% with 80% of kill effort put on legacy. This is a more sustained effort (since money applied to refactoring is not applied to adding new software assets). The complexity ration evolves from 0.5 to 0.464.

- The “careless” scenario is defined by N% = 5%, K% = 3% and R% = 30% and clean = 5%. These values are quite representative of most IT strategies (cf. what we said earlier, 30% of renewal is already the sign of a managed portfolio, many companies suffer from worse accumulation). Here the complexity moves from 0.5 to 0.509

These simulations are only proposed as an

illustration. What can be learned through repeated simulations is similar to

what we said in Section 2:

- Efforts to clean up the portfolio, to keep the age and the complexity under control, are long-term efforts but they have lasting effects.

- Accumulation in complexity, as well as accumulation in weight, has the dual effect of increasing the run costs and reducing the agility (the effort to change the information system to add new capacities becomes higher).

- Contrary to section 2 and 3 where the models may be calibrated with well-known unit costs, measuring the negative effect of complexity and the positive effect of refactoring is hard. What is proposed here is a simple and conservative model that has the benefit of showcasing the effects of both but finding the right constant /parameters to match this model to your reality requires efforts and will lead to some “guesstimates”.

- The key benefit of keeping weight and complexity under control is to allow for a higher refresh rate, which is itself a business imperative which can be modelled through “value decay” (Section 4). In order to simulate the value created by an aggressive “keep the complexity under control” strategy, you need to work under the situation of strong need for refresh (high decay). The weight of technical debt becomes a huge burden as soon as the environment requires to constantly update the information system.

6. Conclusion

The title

for this blog post is: “Managing

Complexity and Technical Debt: A Model for Quantifying Systemic Analysis”.

There are two key ideas here : the first

one is “quantifying” and the second one is “systemic”. Both are related to the

fact that this proposed model is foremost a communication tool. I decided to

build a quantified model because this is the best way to communication with

business managers. It does not mean that this model should be used for

forecasting future IT costs, it is by far to simplistic. Using models and

simulation is a great way to communicate with CFOs; they are even more

effective if they rely on simple parameters/KPI such as unit costs that can be

evaluated through benchmarking (cf. the Gartner

paper on how CIOs can work with CFOs). To make this communication tool work

for your case requires using your own data, as was said repeatedly.

The second

benefit of working with a model is the benefit of simulation, which is a free

benefit once you have built your own spreadsheet. Being able to play “what if”

scenarios is critical to help your stakeholders understand the systemic nature

of the IT costs:

- Delays: good decisions may have long delays before showing their positive consequences

- Accumulation: this is the main difficulty of managing information systems, once the cost problems are visible, they are much harder to solve.

- Amplification (reinforcement): bad decisions produce waste that adds to the complexity and the overall weight, producing further problems along the way.

Although the topic is very different

from the topics that I have covered using GTES

(Game Theoretical Evolutionary Simulation), one can find the same pattern : a

simple model is used to create simulations that are organized into a serious

game from which systemic insights may be gained. As was stated earlier, the goal here

is not to define the “best IT asset management strategy” using a crude model,

but to gain a systemic understanding why long-term complexity-constrained asset

management policies must be implemented.

Here are the conclusions that I can

draw from playing with this generic model (more detailed conclusions would

require working a on a specific instance):

- Keep the age of your software assets under control

- Keep the scope as small as possible (but not smaller, to paraphrase Einstein)

- Constantly refactor your information systems, at different scales.

1 comment:

Interesting Post. I was looking for Biology Lab Instruments Supplier and I reached here. I thought this is such a nice concept and will help me for my search.

Post a Comment